Group Health Insurance vs Individual Health Insurance: Key Differences Explained

Mar 25, 2026

PNN

New Delhi [India], March 25: Individual and group health insurance are two common ways to manage healthcare costs, but they work in very different ways. Each option differs in cost structure, flexibility and how coverage is accessed. Understanding these differences and eligibility rules, as well as certain considerations, helps in deciding which option aligns better with business needs and workforce requirements.

What is Group Health Insurance?

Group health insurance is a policy offered by an employer to cover employees under a single plan. It usually includes basic health benefits and may also extend to employees' dependants. The employer selects the insurer and plan structure, and usually pays a portion of the premium. Coverage is linked to employment and mostly ends when the employee leaves the organisation.

What is Individual Health Insurance?

Individual health insurance is purchased directly by an individual for personal coverage. It allows for greater flexibility in choosing the sum insured, benefits and add-ons. The policyholder pays the full premium and remains covered regardless of job changes. This option gives more control to the insured over health coverage.

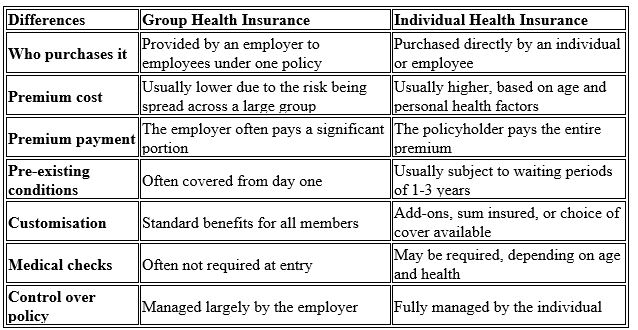

Key Differences Between Group Health Insurance and Individual Health Insurance

Here are some differences between individual and group health insurance policies:

Benefits and Limitations of Group and Individual Health Insurance

Each type of health insurance comes with its own advantages and limitations. So it is essential to understand before making a choice:

* Group Health Insurance

Pros

* Lower premium costs due to risk sharing.

* Employer contribution reduces the cost burden.

* Pre-existing conditions may be covered from the start.

Cons

Group insurance is tied to employment, which means coverage may end if the job changes or employment stops. The benefits are usually standardised, offering limited flexibility or scope for customisation based on personal health needs.

* Individual Health Insurance

Pros

* Greater flexibility in choosing coverage and add-ons.

* Portable and renewable for life.

* Independent of employment status.

Cons

* Individual health insurance often comes with higher premiums, as pricing is based on personal factors.

* Waiting periods may apply for pre-existing conditions.

* Some policies may require medical tests before approval.

Conclusion

Choosing between group and individual health insurance depends on how coverage aligns with work arrangements, financial planning, and long-term needs. A group health insurance policy works well as long as employment continues, but it may not extend beyond that phase. Individual health insurance fills this gap by offering continuity and control when circumstances change. This is why maintaining active health insurance helps ensure access to medical care without delays or unexpected expenses. Review your coverage options and stay insured to support healthcare needs at every stage.

(ADVERTORIAL DISCLAIMER: The above press release has been provided by PNN. ANI will not be responsible in any way for the content of the same.)